Natick, Massachusetts – December 15, 2006 – The growing complexity of today’s embedded software and systems has driven many developers to consider a model-driven development strategy.

Recently published research by Venture Development Corporation (VDC) indicates that more developers are expecting to adopt model-driven development approaches, including UML, over the next two years to cope with this complexity and an increase in the lines of software code per device.

However, increased adoption of software modeling tools has not translated into equivalent increases in commercial market revenue to the degree that VDC had previously anticipated. VDC suspects that a number of factors, including the availability of low-priced UML modeling tools, have significantly impacted the growth of the commercial market for software-modeling tools.

According to Matt Volckmann, Senior Analyst from VDC’s Embedded Software Practice, “Within the embedded UML market, numerous lower-priced commercial alternatives have appeared.

VDC believes that providers of these lower-priced tools are offering solutions that are adequate for the needs of developers that have fewer highend requirements.”

VDC expects continued adoption of model-based development tools, as the benefit of modeling complex systems helps developers to organize and manage complex software and system development. These tools currently see the most use in the early phases of the design process. However, as adoption increases and leading suppliers continue to advance their solutions to drive modeling environments to the center of the development process, VDC expects additional users to more readily acquire additional tool extensions with increasingly sophisticated capabilities.

One of the keys will be to understand the requirements of new adopters in order to capture additional share. According to Volckmann, “Findings from our end-user research show that early adopters of design automation tools (those currently using these technologies) have quite different characteristics than the group of developers yet to adopt these types of tools.”

Within the Volume IV: Embedded Design Automation and Simulation Tools report, VDC offers several strategies for commercial software modeling tools suppliers in the embedded market to effectively compete within this emerging UML space. In addition to software modeling tools such as UML, this report also includes analysis of other modeling and simulation technologies in current use within embedded development, many of which have seen more steady commercial revenue growth.

Friday, December 15, 2006

UML Design Tools Market Continues to Face Competitive Pressure from Low-Priced Alternatives

Thursday, December 07, 2006

GHS Technology Conference – December 2006

VDC attended the 4th annual GHS Technology conference in Santa Barbara, California last week. This show is hosted each fall by Green Hills Software (GHS) and features presentations from the company’s internal development team, industry end users, and a variety of embedded software market leaders and experts. The show again provided valuable information on some of the key trends in the embedded market and updates on Green Hills Software’s latest capabilities. This bulletin presents a summary of the event.

It’s all about security…

Green Hills’ Dan O’Dowd kicked off the show with a thought-provoking discussion on how security attacks are on the rise, how both embedded and non-embedded software in current use has done little to prevent determined attacks, and how device vulnerabilities across all categories threaten the reliability of these systems – ultimately leaving the public at risk. This presentation set the tone for the entire show, as Green Hills continued to demonstrate the areas in which it has focused on building advanced security features around its entire product line, and certifying its software to the highest security standards.

Key Technology Exhibits

As the key theme of the show centered on security and its importance to all markets, one of the first announcements was the release of the Green Hills Platform for Secure Networking. This platform is oriented at a number of device types, from network infrastructure to consumer electronics, and is based on the MILS (Multiple Independent Levels of Security) separation kernel technology within the INTEGRITY operating system. The platform is designed with a number of key security features including guaranteed resource allocation, application partitioning, access control, and others.

In addition, the company reviewed and demonstrated a number of key product announcements and technology developments that have occurred over the past year. Some of the key product milestones in 2006 included:

– The release of version five of GHS’s MULTI development environment, including:

- The DoubleCheck static analysis tool

- The Distributed Build technology, allowing companies to use processing power across their development workstations to speed compile/download times

- Fast virtual hardware simulation

- Advanced visualization and analysis capabilities

- New tools for improved multicore development

– The release of the 10th Anniversary Edition of INTEGRITY, which Green Hills expects to be the first operating system to be evaluated to EAL 6+ in early 2007. Some of the latest improvements include:

- Support for non-uniform memory architectures (NUMA) and symmetric multiprocessing (SMP)

- A new “pure virtual” device driver for improved security, reliability, and safety certification

- A new “debug agent” and “kernel aware” debugging through the integrated MULTI 5 environment

– Green Hills Software’s release of the new ultra-small footprint operating system, µ-VelOSity.

– Enhancements to the TimeMachine product line including TraceEdge-PCI, TraceEdge-PMC, and In-Memory Time Machine capabilities

– POSIX certification for INTEGRITY Workstation

– The release of the Enhanced Platform for Automotive Systems

In addition to these and other product announcements, discussions, and demonstrations about Green Hills Software’s technology, the two day event also included presentations from a number of clients and independent experts. Some of the most interesting included a presentation from the IPv6 Summit discussing the opportunities that will result from the rollout of the “new Internet” through IPv6, and a presentation from the Idaho National Laboratory on efforts to protect infrastructure critical to national security.

VDC’S THOUGHTS ON SECURITY IN THE EMBEDDED MARKET

In today’s international landscape of terrorism and ever-advancing network connectivity, security certainly should have strategic relevance to all companies building embedded devices. Recent accounts of security attacks and the level of vulnerability across most of today’s computing systems will make security one of the more critical challenges faced by device manufacturers over the long term.

The key question is whether the problem of security vulnerability currently represents the primary concern of today’s computing manufacturers. Surely, within key verticals such as aerospace and defense, where security is more akin to reliability, this is currently the case. In addition, within networking and telecommunications, this is becoming an even more relevant issue. However, in other markets, VDC suspects that there is less attention paid to security than other pressing development requirements, perhaps to the detriment of the end user. VDC believes this will likely change over time, however, several factors could drastically change the level of focus on security in the short term:

- An acute, large-scale global security event

- Government mandate(s)

- Drastic increases in security attacks directly impacting device manufacturers financially, possibly through:

- Law suits,

- Disruption of services, and/or

- Loss of current or potential customers.

In the absence of such catalysts in the short term, the goal of improved security may continue to receive second billing behind other factors on the minds of developers such as development cost, time-to-market, and inclusion and integration of new device features.

Fortunately for Green Hills, the company continues drive toward improving the quality of its development tools across these other areas as well, with new development tools and platforms offering more efficient development, a royalty-free real-time operating system, improved support for multi-core environments, hardware simulation, testing and debugging, and many others. As a result, many companies may ultimately select Green Hills’ solutions for reasons other than security, and later on down the road be glad that Green Hills had the foresight to be thinking about embedded device security.

ALSO SEE

Richard Goering’s Article on the event in EE Times

Wednesday, November 29, 2006

Safety- and Mission-Critical System Development Continue to Drive the Market for Test Automation Tools

Natick, Massachusetts – November 29, 2006 – Technology advances have enabled device manufacturers to introduce a wide variety of functionality and features in an ever-expanding universe of computing platforms. The demands for increased functionality are driving the volume and complexity of code that needs to be developed and tested, which is adding more pressure to shrinking product development cycles.

Recently published research by Venture Development Corporation (VDC) indicates that more than 70% of embedded developer survey respondents using Testing Automation Tools in their current development project are in industries normally associated with safety- and mission-critical requirements.

According to Steve Balacco, Senior Analyst of VDC’s Embedded Software Practice, “Device development with safety- and mission-critical requirements have a more rigorous development and testing process and certification through regulatory agencies where required. In other industries, product development is willing to take on some level of risk for latent software defects in the face of getting to market quickly and managing product development costs when compared to harm to the manufacturers reputation, litigation, and costly recalls.”

As the volume of software code has proliferated and project schedules shrink, development organizations no longer have a sufficient number of staff to identify damaging defects in the code in a cost-effective manner. Increasingly, development teams are relying on more sophisticated test automation tools including static analysis tools to identify code defects and security vulnerabilities earlier within the development process to reduce the cost and time in fixing defects on the backend of the development process.

From VDC’s perspective, there is no silver bullet since bugs and flaws are not limited to the actual code developed but also can be discrepancies related to requirements or design, or the customers’ expectation of how the device is intended to perform.

According to Balacco, “VDC expects that as the level of risk increases in industries beyond safety- and mission-critical device developers will look to leverage the experience and knowledge of these markets as a competitive advantage in improving quality, reliability, and the business-critical nature of devices developed.”

Tuesday, October 10, 2006

VDC Launches Study on Electronic Systems Level (ESL) Tools

VDC has launched its 2006 global market analysis of Electronic Systems Level (ESL) Tools. This study will provide answers to critical questions about the competitive landscape, customer requirements, profitability, and strategy within the ESL space. VDC currently defines ESL as a development methodology using abstract modeling or system description language (often on a higher level than RTL) to design an embedded system. ESL tools can be used to design, prototype, verify, debug, and virtually simulate embedded hardware and systems. These tools are often used in the development of SoC and/or multiprocessor architectures, and may also enable the advanced development of software running on these systems.

The founding sponsor discount period has been extended to November 15th, 2006. Sign up now to take advantage of the survey guide review process that takes place during October and November. Make sure your views and questions are considered for inclusion in the 2006 survey guides for this study.

VDC will be looking to founding sponsors to offer early guidance on market and segment definition and product identification. These companies will also have the greatest influence on the primary research process. VDC believes that participation in the development of the infrastructure development phase of the research will bring added value to its clients. Founding sponsors will have early access to key content not available to purchasers of the final report, including:

· Vendor product lists

· Infrastructure documents

· Interim findings

As this is the first report VDC has conducted in the ESL space, VDC looks forward to working collaboratively with all vendors and industry participants. The ESL tools market touches on both the EDA and embedded software development tools markets. There are varying opinions among market participants regarding the boundaries of the market. There are also many questions about future demand for these products, rates of customer adoption, and evolving business models.

While initial advances into the ESL domain originated out of the EDA market, VDC has witnessed increased vendor activity in the embedded software development market as well. VDC believes that a number of market dynamics within the embedded systems industry are driving interest in tools that enable better defined practices and tools to develop software and hardware in a more collaborative and integrated approach. Several of these factors include:

· The increasing density/complexity of silicon architectures requiring tools to facilitate the design of these systems at higher levels of abstraction.

· The growing interest in the development of complex multiprocessor/multi-core system designs.

· The growing role of software development as a key part of the device development process.

· The desire to enable the parallel development of software before the hardware is available.

The term “ESL” represents a broad set of technologies and is not particularly well defined in the eyes of many in the software industry at large. VDC looks forward to working with its research partners to design primary research infrastructure (targeted at the vendor and end-user communities) that addresses key questions and perspectives relevant to the ESL market.

Saturday, September 30, 2006

Embedded Boards Review – ESC Boston 2006

The Embedded Systems Conference Boston 2006 was well attended for what we have come to expect from the Boston show. Many vendors that VDC met believed the quality of the show was up and show organizers indicated that both registration and attendance were up. Exhibitors said that meetings and discussions were leading to serious talks and actionable ideas about how their products could be built into systems. Attitudes seemed upbeat and it seems not only the show, but the embedded space as a whole, are generating some momentum.

VDC believes that a key reason for this success and the increasing activity of people in the aisle ready to find new products has in large part to do with RoHS. RoHS has led to pent-up demand in the market that is now being released. When RoHS was first announced, it was not clear what would happen with the directive. The market was not sure if it was for real or if it was something that would fall by the wayside. It is known by now that it is in fact very real and will not go away. Even though this has been evident for some time now, people were skeptical about the first products that would be RoHS-compliant.

For RoHS these were very real concerns due to the tin whisker problems associated with lead-free solders and other durability concerns. For these reasons, it is likely that many people who knew they had a new product development or launch coming up in the timeframe of the launch of RoHS delayed these to avoid falling prey to the pitfalls of being a first adopter. Now the many RoHS-compliant product releases that have come leading up to the July 1, 2006 deadline are alleviating fears to a certain degree. They are beginning to buy components again to launch their own development efforts that had been delayed while they waited to see what would happen with RoHS. VDC believes this was partly responsible for some of the action at the ESC Boston show this year.

THE BEST OF BOSTON

Show

Ampro Computers – The PC/104 stackables and embedded motherboards specialists had the first EPIC Express board at their booth that VDC have seen. It was also the only EPIC Express board on the show floor. We have all known that EPIC Express was coming for some time and many vendors are scrambling to soon release these products, however it appears that Ampro will be one of the first to market with a product. This begins a new generation of innovation for Ampro as they look to be technology leaders with other upcoming solutions such as PC/104 Express.

Demo

It’s about time that a vendor had an exciting demo that peaked the crowd’s interest on a grand scale. This year the clear winner in the best demo category was Sun Microsystems with its large model race track, complete with dueling race cars speeding around the track. We’re sure this was a strong attraction to Sun’s Java exhibit.

NOT SEEN ON THE FLOOR

The notable absences from the show on the embedded hardware side of things were Motorola Embedded Communications Computing (MECC), Radisys, Trenton Technology, Diversified Technology, and Performance Technologies, who did not have booths in the exhibition. As a side note, on the software side many people were talking about Wind River’s absence from the show.

SEEN ON THE FLOOR

VersaLogic had on display the first COM (Computer-On-Module) on an embedded motherboard that we’ve ever seen. A COM for active backplanes (motherboards) is a product that we have expected to see for quite some time now – from anybody. It looks like it will be a successful product for them, giving customers many options to switch in and out different processors without having to buy an entirely new motherboard.

Intel made an announcement during the show that they will be extending the life-cycle support for the Intel Core 2 Duo E6400 and T7400 processors for embedded applications to 5 to 7 years. This is aimed at meeting the unique requirements of embedded customers.

AMD was at the show with the message that they intend to place a greater focus on the embedded market moving forward. Similar claims have been made in the past and only time will tell if this really happens, but it appears that AMD’s intentions are genuine. AMD can now offer very real advantages to embedded customers with low-power processors and the ability to integrate video onto chipsets.

VIA Technologies announced the release of an HDTV ready chipset for the embedded market at the show. The chipset is for the VIA C7 and Eden processor platforms and it integrates graphics, audio, memory, storage, and HDTV support all in a single chip design. It appears that the processor and chipset supplier will be targeting the embedded market with integrated products such as their Mini-ITX and Nano-ITX motherboards that offer customers an entire integrated board, processor, and chipset solution.

Advantech is making a push toward integrated embedded computer systems by leveraging their knowledge and expertise in boards to build quality integrated systems around their many board offerings. They were trumpeting their ARK systems as well as a new system that can be used to support high-def graphics on a variety of screens. A major application of this platform will be to put high-definition advertising up on a flat screen display or television. It seems that there would be high demand for such products from store owners and retailers who want to distribute information around their stores or to advertise in-store.

Digital-Logic is well on their way in developing a PC/104 Express standard. We have heard from the industry that there are a few stumbling blocks currently in the way that have been realized as a result of what has been done with the EPIC Express standard, but Digital-Logic seemed upbeat about the prospects for a standard in the not-too-distant future.

Win Enterprises displayed an interesting IP PBX 1U off-the-shelf platform called WIN CAP (Converged Application Platform). This product provides a cost-effective, scalable, and simple-to-use IP PBX platform that customers can use to also take advantage of a reduced time-to-market as compared to developing a proprietary system from scratch.

The small venture-backed start-up CorEdge Networks was featured in CMP’s Disruption Zone, covering companies with technology or business plans/models disruptive to the embedded market. CorEdge Networks is offering their proprietary Bit Stream Processor chip-level hardware and software technology on AMC cards that allows for networking applications to operate at 10Gbps. This firm is focused on the AMC and µTCA segment to distribute their IP, which is in their ASICs.

Friday, September 29, 2006

Embedded Systems Bulletin – September 2006

VDC attended the 2006 Embedded Systems Conference in Boston this week. This bulletin presents a summary of the event.

Embedded Systems Conference – Boston 2006

With several of the leading embedded software vendors again taking a pass on exhibiting, this year’s ESC Boston show played out as most anticipated. The Boston show in some ways has established itself as the lesser of the two annual ESC events; however, most attendees and exhibitors seemed satisfied to get about what they expected out of the week. There was a mixed reaction from most vendors on traffic, but more exhibitors than not commented that the quality of the leads from the show exceeded previous years, as well as in some cases, the ESC/San Jose conference held earlier this year.

THE “EMBEDDIES” GO TO:

Best of Show

Telelogic/I-Logix – The makers of Rhapsody have done it again with the release of 7.0. The latest version of the company’s model driven development environment is a testament to the company’s relentless determination to improve their product and drive innovation in the tools market. One of the most interesting new features is a new integration with the The MathWorks’ widely popular Simulink tool suite. Developers can now import Simulink modeling blocks into the Rhapsody environment, enabling them to accomplish tasks previously requiring manual interfaces between the two. With a number of other improvements such as features that allow developers to work in a more “code centric” environment and new add-ons enabling enhanced mechanisms for code reuse, the company continues to establish itself as a clear market leader in embedded model driven development. For more information visit: http://www.telelogic.com

Best Demo

It’s about time a vendor had an exciting demo that entertained conference attendees on a grand scale. This year the clear winner in the best demo category was Sun Microsystems with its large model race track complete with dueling race cars speeding around the track. We’re sure this was a strong attraction to Sun’s Java exhibit.

Key Announcement

With well-placed banners and a clear message, Mentor Graphics announced that they would be reducing the price of their EDGE development tools to $2,995 per seat. The announcement should be seen as a clear indication of the pricing pressure that may continue to impact the market going forward. With its corporate strength residing in the EDA market and a history of not hesitating to aggressively compete on price in other instances, VDC believes that other vendors in the market should not fail to take note of Mentor Graphics’ latest movements. In dropping the price of its EDGE development tools, the company is clearly throwing down a challenge to other commercial vendors to justify charging more for their operating systems and tools and demonstrate the additional value they can provide. The company complemented this significant announcement with additional improvements to its Nucleus operating system and a key partnership with STMicroelectronics and the Nomadik product line. VDC expects this partnership to further support Mentor Graphics’ push into the application processor segment of the mobile phone market, where the company already has dominance around the requirement for baseband processor operating systems.

Ensuing Pricing Battles in the Operating System and Development Tools Market

Mentor Graphics’ announcement was part of a larger theme VDC observed at the show. It is increasingly clear that many suppliers are determined to offer quality, commercial-grade development tools at significantly lower per seat prices. These efforts are rapidly shifting the value of software solutions higher up the stack. Consequently, leading vendors are pushing to deliver solutions to market that provide a much broader level of value than before, in order to effectively compete for high-end customers and encourage embedded systems manufacturers to standardize on their software solutions.

WALKING THE FLOOR

ENEA announced version 2.0 of its Element High Availability middleware product that uses Enea’s LINX communications services and supports a number of Linux operating systems and AdvancedTCA systems. The company also revealed an Eclispe-based IDE to support its OSE RTOS called Optima starting at $3,000 per seat.

Green Hills Software demonstrated its commitment to bringing more function into its MULTI tool chain with the introduction of MULTI 5.0. The release included a major upgrade to TimeMachine, a source code analyzer called DoubleCheck, a distributed project builder, and a high-speed system simulation tool. The company also announced a new version of its GHNet TCP/IP networking software and the availability of SuperTrace probe and TimeMachine for Freescale’s ColdFire microcontrollers.

After celebrating a 10 year anniversary, Express Logic announced ThreadX RTOS support for Tensilica’s Diamond Standard and Xtensa processor cores. Marketing VP John Carbone also participated in a “No BS” panel discussion on the use of Linux in real-time and embedded systems. The premise of the panel was based in part on recent research findings from CMP that the use of Linux in the embedded market is on the decline (research that contradicts VDC’s latest findings).

IBM Rational was also in attendance with demonstrations of its new Eclispe-based Rational Systems Developer product released early this year. The software modeling leader continues to highlight its focus on the systems market and the benefits of an integrated set of life-cycle management tools.

LynuxWorks announced that Dr. Inder M. Singh has assumed the role of company chairman, with Gurjot Singh replacing him as CEO and president. In addition, LynuxWorks made several other announcements at the show including the release of LynxOS-SE, a new partitioned real-time operating system based on the LynxOS-178 product line. The new product offers POSIX and ARINC compliance and an ability to run Linux applications in safety-critical applications. Lynuxworks also noted complete support for Xilinx 32-bit processors with its LynxOS product and announced that RTI’s Data Distribution Service middleware would be ported to the new LynxOS-SE product.

RTI also had a number of announcements including the release of the RTI Data Distribution Service version 4.1 with enhanced messaging QoS and the introduction of its own tool suite called the RTI Developer Platform. The company also announced a partnership with up-and-coming modeling tools vendor Sparx Systems, an emerging provider at the low end of the market.

In addition to announcing its platform partnership with Wind River Systems and one of its recent design wins in the industrial automation market, Aonix announced ObjectAda Real-Time RAVEN’s availability for SYSGO AG’s PikeOS product, which also uses software partitioning to enable safety-critical certification and the introduction of Linux applications.

This year, VDC and Adams Capital Management sponsored CMP’S “The Disruption Zone,” a group of companies with the potential to “propel the next big leap forward in the embedded market.” In addition to grouping these companies in a single location on the exhibit floor, the area featured an event where these suppliers could discuss the details of the unique opportunities that their products offer.

Encirq, participating as one of the nine identified Disruption Zone companies, announced the release of DeviceSQL 3.0. Virtutech, the supplier of full system simulation development tools aimed at accurately simulating hardware to enabling better software and systems development, was also attended as member. Other Disruption Zone members included CorEdge Networks, Enpirion, SecureRF, Sensor Platforms, Quantum Leaps, Quickfilter Technologies, and UltraCell.

The Embedded Business Group of Hitachi America announced the launch of Entier, a new relational database management system for embedded devices. The small footprint database (less than 1MB) offers advanced spatial, contextual and incremental text search capabilities. The solution is particularly suited to address the GPS navigation, set top box, and mobile phone markets, but the company also expects to serve additional markets going forward.

McObject announced a partnership with eCosCentric where McObject has ported its eXtremeDB in-memory embedded database to the eCosPro developers’ kit for the eCos open source RTOS. In addition, the company announced the availability of Perst Lite, a micro-footprint version of the Perst open source, object oriented embedded database.

MaCraigor Systems announced the availability of usb2sprite, the companies USB 2.0 interface product, for Coldfire and DSP 56300 processors and the now company has support for these microprocessors within its GNU toolset, with sample configurations for standard evaluation boards.

Grammatech, the provider of code analysis tools, released CodeSonar 2.0 with added C++ support and the ability to analysis source code larger than a million lines of code. The company also signed agreements with UK-based Scientific Computers and MDS Technology of Korea to distribute its technologies abroad.

Microcross announced that they had entered into an integration/distribution agreement with TrollTech to integrate and resell Qtopia along with its own Linux-oriented GNU X-Tools product.

Other embedded systems vendors also in attendance at the show were American Arium, Ardence, Carbon Design Systems, Coverity, Ember, IAR Systems, IBM Rational, Keil (an ARM company), Lauterbach, Klocwork, LDRA, Microcross, MKS, Perforce, Polyspace, Sophia Systems, Quadros, and others.

Monday, September 25, 2006

GE Fanuc Embedded Systems Continues Full-Out Assault on Military Embedded Market with Plan to Purchase Radstone Technology

GE Fanuc Embedded Systems, a unit of General Electric Company (NYSE: GE), announced on Friday that it has agreed to acquire all of the issued and outstanding shares of Radstone Technology, PLC (London Stock Exchange: RST) for a total consideration worth approximately £130.4 million pounds (approx. US$ 247.8 million). The deal has sixty days from the filing of the paperwork to officially close. This comes after GE Fanuc Embedded’s acquisitions of SBS Technologies and Condor Engineering in March of this year.

1. Why does the timing of this deal make sense for GE Fanuc Embedded Systems & Radstone?

2. How should we evaluate this transaction?

3. What does the deal mean for the competition?

Why Does the Timing of This Deal Make Sense for GE Fanuc Embedded and Radstone?

• Segmentation Growth Through Acquisition – This agreement to purchase Radstone Technology is in line with the strategy that GE Fanuc Embedded Systems has followed in the embedded systems market since the inception of the group with GE Fanuc. This strategy has been to increase the firm’s product portfolio and market share through the aggregation of niche players. The Embedded Systems unit of GE Fanuc was born through the acquisition and merger of three embedded computing companies – VMIC, RAMiX, and Computer Dynamics, with the VMiC Huntsville, AL office becoming the home office. In March of 2006 the business unit continued down this path with the purchases of Condor Engineering and SBS Technologies. Following this round of consolidation the headquarters of the GE Fanuc Embedded Systems business unit moved to the Albuquerque, NM office of SBS, where it currently resides. The plan to purchase Radstone Technology, the high-end conduction cooled VME boards specialist, is just the latest niche player acquisition by GE Fanuc Embedded Systems in a broader effort by the firm to grow the firms product portfolio, particularly focused on growing in the Embedded COTS Military/Aerospace market.

• A Good Time to Sell – Word was widespread that Radstone Technology was in play. A glance at the firm’s financial position makes this pretty obvious. The firm had two years of double digit growth in a row, growing 14% from fiscal 2004 to fiscal 2005 and 10% from fiscal 2005 to fiscal 2006. In 2004 and 2005 the firm showed strong operating margin at 17.8% and 19.0%. The embedded COTS market had averaged roughly 6% growth from 2004 to 2006, so Radstone was beating the market, while also showing strong profits. This made it a great time for Radstone to sell in a hot defense/military market full of potential suitors looking to acquire a new piece of the market.

Given Eurotech’s failed effort to acquire Radstone Technology only a week before GEFE, it would appear that there may have been a mad rush to grab what was an available, sizeable, and desirable niche military COTS embedded company. This market is so fragmented that sometimes the only way to make any order of it and to retain steady market share is to do a tiny piece of the market better than anybody else.

How Should We Evaluate This Transaction?

VDC believes that this deal fits neatly within the GE Fanuc Embedded model: growth through acquisition. With Radstone, GE Fanuc Embedded has filled out its line card in a core product offering, gained access to additional smaller lines, and likely found itself a few dozen additional defense programs to manage and leverage. We think that Radstone and the larger GE Fanuc Embedded business will continue to grow in the near term, throughout the integration transition, and likely beyond.

However, there are a number of questions that remain for us:

1. Assuming (a) certain cost reductions and efficiencies were part of the deal justification, and (b) Radstone’s business is as personality and relationship driven as the rest of the embedded COTs market, how will GEFE meet the productivity goals without eroding some of the most valuable parts of the deal?

2. How will GEFE market, sell and support its growing business of COTs products – as each of the recent acquisitions is built on differing go-to-market strategies?

3. Will GEFE be able to stitch all of these businesses together technically as well as commercially?

VDC believes that the integration of valuable components into higher-value-added subsystems could be an even more significant opportunity – the whole may be a more valuable proposition than the sum of the parts.

Can GEFE position itself as a leading supplier of merchant embedded computing/ communications/control/ countermeasures (EC4) to defense mezzanines? Primes? And what of the larger industrial and commercial market segment opportunities such as IP telephony and instrumentation?

Will software – middleware, utilities, horizontal embedded applications, etc – be part of the GEFE strategy? Our market analysis continues to suggest that higher-level system management, including high availability (HA) support – will be a source of pressure and tension for companies focused on providing discrete hardware platforms.

We like the deal. We are optimistic about the role GEFE might play in the COTs and larger embedded market. We do have questions about where this business ends up.

What Does This Mean for the Competition?

In terms of the overall market for embedded COTS Systems in military applications this is a somewhat small transaction because the market is so broad and wide open. Especially given that there is an increasing amount of participation of the Prime Defense Contractors in this market, weather this be outside sales or just sales to another business unit within the parent company. The market is also flooded with large systems integrators such as HP and Dell as well as large embedded suppliers like Motorola Embedded Communications Computing who do not super actively participate in the military COTS market, but will occasionally supply a custom military product slap a part number on it, put it up on their website, and call it COTS. For these big boys, especially the Primes and the large Systems Integrators this deal may seem somewhat insignificant.

However, this deal does have major implications for the traditional embedded military COTS systems suppliers, these companies often sell to the Prime Defense Contractors Mercury Computer Systems and Curtiss Controls. Theses two companies have in the past been the leaders of this market.

In the recent past, the military embedded market is no stranger to consolidation, as evidenced by the many recent acquisitions by Curtiss Wright Controls and Mercury Computer Systems as well as GEFE’s previous moves into the market.

GE Fanuc Embedded Systems is certainly not buying the market or becoming the first 900 lb gorilla among the niche focused on the embedded military marketplace and selling to the Primes. More to the point, the company has now made itself a more formidable competitor to embedded COTS industry mainstays such as Curtiss Wright Controls and Mercury Computer Systems. Curtiss Wright and Mercury remain the niche leaders for the time being and have set the standard that GEFE is now better positioned to meet. By no means will GEFE now be able to easily win out over the competition; the firm will be in a tough battle with Curtiss Wright and Mercury. We should also not forget that at first anyways, GEFE will be slightly hindered by the integration efforts that it will take for them to combine all of their recent acquisitions into one unit. This should be roughly a one-year effort that will be a slight hindrance and one that will not be faced during the same period by their competitors. There is no reason to believe that at this time the embedded COTS market niche that these three firms compete in can not support all three, along with the many, many other even smaller niche players such as Aitech, Spectrum Signal Processing, and Octagon Systems who are all the experts at what they do.

An interesting development to track as a result of this purchase is the activity of private equity in the market. When Eurotech was not able to acquire Radstone outright, they began a hostile takeover and purchased 15% of Radstone, which means that GEFE will now have to buy back those shares at a gain of a couple million dollars for Eurotech. The embedded market was one where private equity was already ticking up, and when they realize the money Eurotech was able to extract in a very short period of time, it will most likely advance the desires of private equity in the market.

Look for more industry consolidation to occur in the future. With Eurotech losing Radstone to GEFE, look for them to make a move if they really want to bolster their current holdings of Parvus and Arcom in the embedded military market. If the right opportunity appears, Curtiss Wright could go on a buying spree again as well. With involvement of the Prime Defense Contractors in this market and the segmented nature of the embedded COTS military market which has created literally hundreds of firms selling embedded COTS products of some sort, the window of opportunity for acquisitions is never closed.

Monday, September 18, 2006

Growing Software Code Base Offers Greater Role for Application

The following arcticle was featured on VDC's website this week:

Software engineering continues to emerge as an increasingly important part of the embedded development process. The complexity of the software development process and the amount of software code per device are growing. As a result, the need to effectively manage device software over the course of the product life cycle, as well as across a company’s product portfolio, is also increasing. At the same time, the majority of embedded device manufacturers are still managing their software using informal methods.

For these reasons, Venture Development Corporation (VDC) sees an emerging role for application life-cycle management (ALM) tools in the embedded development space. VDC defines ALM tools as part of one or more of the following types of software:

• Requirements Management Tools – These tools provide the ability to define and organize project requirements and compare/track the fulfillment of these requirements within software.

• Source/Change/Configuration Management Tools – These tools systematically organize revisions and changes to software, allowing developers to manage and trace the configuration of the software over time.

• Software Modeling or Model Driven Development Tools – These tools allow developers to represent software visually or at a point of organization above the source code level to model software.

• Automated Testing Tools – These tools allow engineers to systematically test their software.

• Project/Portfolio/Asset/Document Management Tools – These tools help to manage project scheduling, documentation, and resource allocation.

In the IT space, the value of commercial tools of these types, provided by companies such as Borland and IBM/Rational, is commonly granted. However, within the embedded space, historically smaller code bases, smaller teams, and a greater focus on the hardware has resulted in the use of more informal methods of accomplishing these tasks. Some exceptions to this rule have been in the military/aerospace, automotive, and medical device markets where average project lengths are substantially longer and the quality of the code has implications for the safety of these devices. However, within other embedded markets, the growing significance of software (VDC estimates that lines of software code per embedded project are growing at an average rate of 46% per year) is also impacting the way device manufacturers are thinking about the need for more robust ALM tools.

Over the last several years, VDC’s surveys of embedded developers have noted some interesting findings on the current use of ALM tools. Some key issues include:

• Within the embedded market, engineers using informal requirements management solutions outnumber those using formal tools. In VDC’s most recent survey of embedded developers, more than 31% reported using informal means (such as MS Word and MS Excel) to track requirements, while approximately 12% indicated that they used a formal requirements management solution.

• A majority of embedded developers are using open source and in-house source/change/configuration (SCC) management tools rather than those from commercial suppliers. With these solutions used in nearly two-thirds of embedded development projects, SCC management tools are among the most widely used type of ALM tool, and are one of the most firmly engrained technologies as a result of their longer heritage.

• Significant numbers of developers expect to be using model driven development methodologies, such as UML (Universal Modeling Language), in the future. In VDC’s most recent study on the embedded market, nearly twice the number of developers indicated that they expect to be using UML within two years as compared to those reporting that they currently use this type of model-based development approach.

• VDC believes that most developers see the value of a tightly integrated set of ALM tools. However, there is less consensus regarding the degree of efficiency that this type of integration enables, and whether the potential gains outweigh the costs of solution integration, current tool investment, and staff retraining.

• Roughly 44% of embedded developers are currently using project management tools. A majority of embedded developers using a project management solution use Microsoft Project.

As the need for ALM tools increases, one of the key questions is what the implications are for commercial suppliers of these tools. In key markets such as military/aerospace, there is already real demand for a sophisticated and integrated set of ALM solutions, and companies are very aware of these requirements in terms of tools budgeting and planning. In other market sectors (such as the growing consumer electronics industry) it is less clear that companies are willing to spend significant amounts on commercial ALM tools, in lieu of finding cheaper alternatives.

Development tools vendors must continue to improve their solutions and support greater integration with leading tools in the ALM suite. Meanwhile, embedded developers and device companies should consider the adoption of more robust software management tools and practices, in order to limit the additional effort required to cope with their growing code bases. VDC believes that whether they are built in-house, obtained from a commercial supplier, or acquired from the open source community, ALM tools will play an ever-important role in assisting developers to effectively manage their software, control costs, and deliver products to market in a timely manner.

Wednesday, September 06, 2006

Competitive Forces on Multiple Fronts Continue to Place Pressure on Pure Play Unbundled Embedded Software Development Tools Suppliers

Recently published research by Venture Development Corporation (VDC) confirms that the market for pure play unbundled software development tools continues to be influenced by the viability and penetration of open source tools, the migration to commercial operating systems, and the efforts from vendors in many adjacent markets to bring more comprehensive, integrated solutions to their customers. VDC defines pure play unbundled (or standalone) software development tools as compilers, debuggers, graphical user interfaces, and other related tools sold separately from the operating system or other products.

VDC continues to see the market impacted by the effort of all participants within the embedded systems market to deliver added value and provide customers with bundled development tools that are more tightly integrated with their own core offerings.

VDC’s recently released study on the software development tools market (which includes other categories like semiconductor IP and debugging hardware interfaces) predicts moderate growth through 2008. However, its research indicates that the segment specifically attributed to pure play unbundled software development tools is expected to grow at a combined annual rate of only 0.6% per year, due in large part to competitive pressures and the continued migration of leading operating system vendors to the bundled tools market.

“The market for embedded stand-alone software development tools continues to demonstrate significant transformation, as current market participants have adapted to customer demands, and complementary solution providers continue to offer alternatives to the use of stand-alone environments,” according to Matt Volckmann, Senior Analyst within VDC’s Embedded Software Practice.

VDC expects that only those vendors that are flexible enough to adapt to new market demands will ultimately survive these effects. “Embedded software development tool suppliers will continue to be pushed by the market to provide complete solutions that span the embedded development lifecycle,” says Volckmann. “VDC anticipates that vendors without a distinctive value proposition or a clear strategy for migrating and integrating with other parts of the embedded device development process will find more limited opportunities going forward.”

VDC has observed this trend for some time within the embedded development tools market.In 2002, VDC wrote a piece entitled “Last One out Turn off the Lights” in reference to the number of stand-alone tools suppliers migrating to other market segments or being acquired by operating system, semiconductor, and EDA vendors. Today, the vendors that remain within the unbundled tools market face even greater competition from these and other areas of the embedded software landscape. The advancement of open software is also playing a critical role in defining the changing dynamics of the market.

For a PDF of this press release, visit:

http://www.vdc-corp.com/_documents/pressrelease/press-attachment-1240.pdf

Friday, August 11, 2006

Jim Turley to Step Down as Edittor in Chief role at Embedded.com

According to a note on the Embedded.com website, a new edittor will be replacing Jim Turley as he looks to devote more time to his consulting business.

New Eclipse White Paper Available at Eg3.com

Eg3.com recenlty released a whitepaper conducted in collaboration with VDC focused on the Eclipse tools market. If you have an interest in the developments in this market, there are some interesting research findings here that you will likely want to see.

Visit http://www.eg3.com/visible to get your copy. Look for future whitepapers VDC conducts in collaboration with Eg3 and other technology publications.

Wednesday, August 02, 2006

VDC's review of the 2006 Design Automation Conference

Click here to see VDC's review of the 2006 Design Automation Conference

Friday, July 28, 2006

Device Software Optimization – Does the Message Resonate with Developers?

Device Software Optimization (DSO) is a term coined and championed by Wind River Systems. DSO is the result of evolving vendor market strategies to meet the ever-changing technology landscape and the needs of developers. It represents a way to communicate their recognition of the complexity of device software development through the availability of broader sets of commercial-off-the-shelf software platforms.

Vendors have spent a significant amount of time and resources in defining and executing on their DSO strategy. Therefore VDC was interested in understanding in year two of DSO the depth and breath to which the message has connected with embedded software manufacturers.

Recently published research by Venture Development Corporation (VDC) indicates that slightly more than 41% of embedded developer survey respondents have at least heard of the term “Device Software Optimization.” However, of these, only about 12% believe they understand the underlying message.

According to Steve Balacco, Senior Analyst of VDC’s Embedded Software Practice, “In year two of DSO we find a mixed understanding for the DSO message within embedded system manufacturers (ESMs). Adding to the confusion by the developer community may be that vendors seem to have slightly different takes on just what is meant by their use of the acronym ‘DSO’ as a means to communicate strategic product and service offerings.”

DSO seeks a comprehensive approach to maximize the benefits and mitigate the downside of various trends within the development process. The compelling message is to empower developers through optimized, integrated solutions or platforms to enable product innovation, accelerate development, manage costs, and minimize risk. As such, vendors become strategic and trusted suppliers of end-to-end solutions.

According to Balacco, “Perhaps this idea of DSO as its own market provides the most confusion for developers and market participants. It may be that changing the mind-sets within these organizations will prove more difficult to achieve than expected and/or that impact has not been sufficiently quantified with respect to ROI and total cost of development.”

From VDC’s perspective, vendors need to inwardly examine their strategies and refine and focus the message so that ESMs can relate to and evaluate the benefits of investing in integrated commercial off-the-shelf software platforms.

Tuesday, June 13, 2006

Green Hills Responds to Express Logic Injunction: "It's okay to completely copy somebody else's interface"

After reviewing the copyright claim issued by Express Logic yesterday, Green Hills called the the allegations that Green Hills had illegally copied the ThreadX API ridiculous. In fact, Green Hills said that it would be allowed to exactly copy the application interface if it wanted as "It's been done many times by everyone in this industry, including Express Logic."

As VDC is not a legal body, we will reserve judgement until the matter has been decided by the arbitrators.

Monday, June 12, 2006

"µ used our APIs!" - Express Logic seeks injunction against Green Hills Software

Today, Express Logic announced that it would would seek to stop Green Hills Software from marketing its small footprint µ-velOSity operating system released in April of this year. Express Logic cited the similarity in the API structure between the Green Hills product (as sourced from a Green Hills Software Evaluation CD) and Express Logic's ThreadX operating system and further contended that the API used in µ-velOSity is a departure from the API structure used in other OSs in the Green Hills family.

These accusations are interesting when considered in conjuction with claims made on the release of µ-velOSity -- with Green Hills explicitly noting that the µ-velOSity product featured "an upward compatible API with velOSity and INTEGRITY." In fact, the idea of being able to write to a common set of APIs as a company scaled its product seemed to be a point of focus upon the release.

In fairness, Green Hills has yet to respond comments regarding the allegations, and any judgement has yet to be decided (Express Logic is opting to settle this matter through arbitration in conjunction with its existing reseller agreement.)

It will be interesting to hear the other side of the story.

Tuesday, June 06, 2006

Toyota to build own operating system

Toyota announced last Thursday that it will be working with Nagoya University to design its own operating system, due for release in 2010, to handle both vehicle control and in-car systems.

Thursday, May 18, 2006

Virtual System Simulation Evolution: Virtio Acquired by Synopsis

On Tuesday, there was interesting news in the ESL space. EDA leader Synopsys announced that it would acquire virtual system simulation player Virtio in a deal valued at around "$15 million depending on 'earnout'" according to EE Times.

With EDA, ESL, and virtual system simulation (VSS) vendors reporting encouraging revenue growth of late, the growing complexity of hardware architectures and increasing role of software development, as well as moves from other industry leaders like CoWare to enable hardware and software design/validation through a common platform, the time appears to have arrived for more unified ESL/VSS solutions.

While both ESL and VSS solutions hold their own value as stand-alone products used in the hardware development and software development processes respectively, the prospect of being able to use a single platform to both evaluate hardware designs and virtually vet software prior to fabricating the physical hardware seems an attractive notion.

Of course the real value in this concept is only realized where companies can get hardware and software development teams to work in a more collaborative way -- something that would be a substantial change from the way that today's embedded products are brought to market. However, this seems to be changing, especially amoung companies on the bleeding edge in time-to-market sentive industries like consumer electronics and telecom.

If, in fact, more unified ESL/VSS development turns out to be the long-term direction of the market, the next logical questions are: how will the remaining standalone VSS leaders be impacted by this type of an evolution, and what steps will the leading EDA players, namely Cadence and Mentor, take next?

Friday, April 07, 2006

VDC's Review of the 2006 Embedded Systems Conference in San Jose

Click here to see VDC's review of the 2006 Embedded System Conference

Friday, March 10, 2006

Samsung Turns to FSMLabs for Linux

FSMLabs continues to add customers and win business for its real-time Linux products. Samsung Heavy Industries is using RT Linux Pro in its shipbuilding robots. Move over Roomba and Scooba the previous most high profile Linux Robots.

Timesys signs up Linux developers

Timesys reports that it has signed up 2,000 developers for its LinuxLink service. LinuxLink is a repository of the latest packages, development tools and other types of community support for Embedded Linux.

Could this signal an upsurge in the use of non-commercial distributions? Perhaps. But it maybe it just signals a change in how those existing developers acquire patches and tools.

Thursday, March 09, 2006

WIND Q4 - VDC's View

Despite the hit that Wind River has taken in the market (down 20% at 2pm), its Q4 and FY06 earnings have many positive components including:

- 1st Quarter over $70 million in 15 quarters going back to Q4 2002.

- Overall Growth of 13% and deferred revenue growth of 27%.

- $50 million in cash flow.

- Many big design wins, especially in military/aerospace.

So what did Wall Street investors not like about the numbers:

- The company missed the low end of its guidance of $72-74 million by turning in a $70.2 million Q4.

- Lower than expected Q1 guidance of $65-70 million or $0.34 to $0.39 per share less than analysts' $0.47.

Other factors to consider in evaluating the numbers:

The transition from paid up front product licensing to a subscription business model will not be always be smooth. In fact, there will be some jumps and some lags in it. This quarter was a jump. More of WIND’s business came in under the subscription model than was expected. Some OEMs in markets that typically prefer PUF, including military/aerospace and industrial automation opted for subscription. Has the inflection point been passed? Not by any stretch but OEMs appear to be considering alternatives to PUF growing numbers.

It appears that some bookings that were expected to be recognized because they would be under the paid up front licensing model were actually puchased under subscription models. Although this hurts WIND in terms of quarterly performance, this is better for the company in the long term. Subscription deals tend to:

1. Be larger deals

2. Lock in customers for the long term

3. Be renewed at higher rates than PUF

4. Include more products and services

5. Be standardization deals

Also mentioned were a number of deals that have yet to hit balance sheet that VDC believes to be quite large.

Bottom Line:

Certainly WIND missed its expected revenue number for the quarter, however there appears to be a number of mitigating factors including growth, cash flow, a movement to customers into subscription licensing which is better for WIND, and a number of deals that have yet to appear in the financial statements. WIND’s results are not simple to understand. They are neither all positive, nor all negative. There are no straight lines here, instead you need to look at all of the information. For VDC, the preponderance of that information is positive.

Wednesday, March 08, 2006

Wind River Post Healthy Gains But Misses High End of Guidance

Analysts had expected the company to earn $0.12 per share on revenues of $74.20 million for the quarter.

Full-Year Highlights:

Reported revenue increased 13% year-over-year to $266.3 million

Deferred revenue increased 27% year-over-year to end at $98.3 million

Non-GAAP earnings per share of $0.29 and GAAP earnings per share of $0.26

Non-GAAP cash flow from operations of approximately $51 million, excluding restructuring related payments of $1.8 million; GAAP cash flow from operations of approximately $49 million

Fourth Quarter Financial Highlights:

Reported revenue increased 11% year-over-year to $70.2 million

Deferred revenue increased 12% sequentially vs. Q3 FY06

Non-GAAP net income of $10.3 million and GAAP net income of $10.3 million

Non-GAAP earnings per share of $0.11 and GAAP earnings per share of $0.11

Non-GAAP cash flow from operations of approximately $16 million, excluding restructuring related payments of $579,000; GAAP cash flow from operations of approximately $15.5 million

(Full VDC Coverage Tomorrow)

WIND Earnings today at 5pm

WIND's share price has been trending in February. Is this a sign of things to come? Not so fast. If you have the time, check in with the price at about 2pm or so (maybe 3pm). There is usually some movement around then...and that movement usually tells us the way things are going.

Tuesday, March 07, 2006

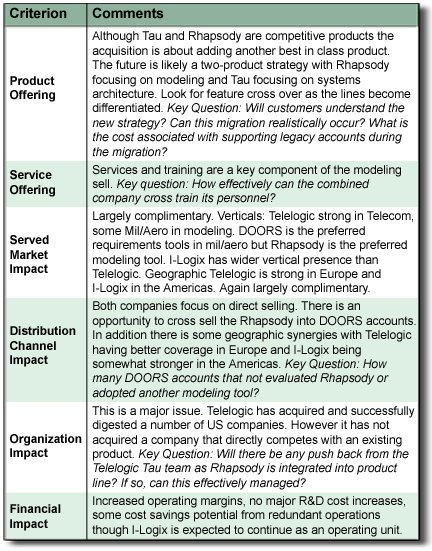

VDC's View Telelogic - I-Logix

The acquisition of I-Logix represents a continuation of Telelogic’s strategy to acquire leading companies in their respective corners of the application lifecycle management business. These acquisitions include:

Popkin (2005) - leader in enterprise architecture modeling (cost: $45 million)

QSS (2000) leader in requirements management tools (cost: $115 million)

Continuus (2000) leader in change and configuration management tools (cost: $42 million)

Other acquisitions include Verilog (SDL), COOL:Jex from Sterling Software (UML), Focal Point (decision management tool), Devisor (consulting) and Certeam (consulting)

Key observations:

I-Logix Rhapsody is likely the best-in-class software modeling tool. The acquisition brings another best-in-class tool into the Telelogic line continuing its successful acquisition strategy.

Telelogic’s transition from SDL to UML modeling has not been an easy one. While Telelogic has enjoyed great success in telecom, its move into other vertical markets has not been as successful. The acquisition brings instant credibility to Telelogic in the automotive, military and aerospace, medical and consumer electronics verticals.

The acquisition establishes the best-positioned modeling company in the embedded business from safety-critical, real-time applications to large systems architecture. The combination of Telelogic, I-Logix and Popkin is the “perfect storm” of software and systems modeling.

The acquisition brings together Telelogic’s strength in building product portfolios with I-Logix’s award winning product strategy. The key component that has been missing for Telelogic in its modeling products for some time.

This acquisition does not sacrifice the innovative relationship that I-Logix has established with Green Hills, which features a tightly integrated IDE/modeling environment.

I-Logix is also working on a partnership with Esterel Technologies to integrate Esterel SCADE certified code generator into Rhapsody. The result for military and aerospace customers could be a near-seamless experience from DOORS to Rhapsody to SCADE Qualified Code Generator (KCG) to Green Hills MULTI (certified by Esterel’s compiler certification tool), all running atop Green Hills’ INTEGRITY OS. Additional support comes from Enterprise Architect and SynergyCM. In addition to the end-to-end nature of the tool chain and the efficiencies of modeling, the benefits of this approach include compiler optimizations for faster, smaller code that is in essence certified by virtue of being generated by the certified code generator. VDC expects that other vertical markets will find this configuration appealing as well.

Bottom line: This is an important acquisition that benefits customers in a meaningful way while at the same time changing the competitive landscape of the industry. This is now clearly a 2-company market and Telelogic has the momentum.

Monday, March 06, 2006

Telelogic acquires I-Logix

What Happened:

Telelogic acquired I-Logix for $80 million in cash. The I-Logix team will form the basis of a new Systems and Software Modeling Division at the company. The new division will manage the Rhapsody, Statemate, Tau and Tau G2 products. I-Logix had sales of $26.8 million in 2005 and pre tax profit of $2.9million.

Embedded World Numbers are in

The participant numbers for Embedded World are in:

Exhibitors: 492

Attendees: 12, 234 (up 22%)

Speakers/Participants: 913 (up 22%)

Awards:

Software: QNX for QNX Multicore

Tools: pls Programmierbare Logik&Systeme for Universal Debug Engine

Hardware: NEC

VDC View: Embedded World continues to grow and maintain its place as the largest embedded trade show, but ESC West remains the most important. Could this change? Sure. But moving to San Jose is likely to boost ESC and help it maintain its importance.

Catch Us at ESC West

Chris and Matt will be at the show. If you would like to schedule time please drop us a line at the office. Email is best. Believe it or not, slots have already started to fill.

The Blog is Back!

On Target: Embedded Systems went to Maui for a couple of weeks and efforts to post from the island or from VDC Global HQ in Natick, MA were lacking. But we are back now. Tanned, Rested, Ready.

Wednesday, February 15, 2006

Access/Palmsource Announce New Linux Platform

At the 3GSM World Congress this week, Access and Access-owned PalmSource announced the availablility of the ACCESS Linux Platform (ALP).

The Rumors Were True: Oracle Moves To Acquire Sleepycat

Yesterday, Oracle definitively announced that it would acquire embedded database vendor SleepyCat Software.

Tuesday, February 14, 2006

Green Hills and Esterel

Green Hills Software and Esterel Technologies are announcing a partnership that will lead to a highly integrated package of products for DO-178B Level A and IEC 61508 SIL 3 applications.

The partnership appears to be modeled on an earlier Green Hills agreement with I-Logix. Indeed I-Logix and Esterel also share are partnership and integrations.

While it is difficult to tell at this point if the partnership is as deep as the I-Logix arrangement. If it is, this could be major step forward for Green Hills in the battle for the military/aerospace market. Green Hills appears to have seen the value in modeling and also in the Esterel certified code generator (KCG). The SCADE KCG produces code that is correct by construction. KCG produced code can avoid the MCDC testing required in DO-178B certification.

This agreement is indicative of Green Hills’ current partnering strategy. Find companies on similar fast growth trajectories that have similar cultures and goals, are market technical leaders and are willing to forge deep connections between products and perhaps organizations.

Other news from Embedded World:

Quadros Systems has ported their convergent RTOS technology to the Freescale ColdFire MCF532x and MCF537x processors. Because Quadros RTXC dual-mode RTOS offers optimized dataflow and control capabilities, it is able to maximize the DSP, RISC and I/O capabilities of these new platforms.

Aonix is announcing SWT graphics extensions for its PERC virtual machine. SWT, a Java-based graphics library and widget toolkit developed as part of the Eclipse platform, is designed to be as close to the native platform as possible, making it ideal for embedded applications. This integration makes Aonix PERC VM increasingly suitable for applications such as avionics, communications, industrial automation, office automation, power plants, transportation, mil/aero, and fleet telematics.

Express Logic, Inc. today announced that Express Logic’s ThreadX RTOS now supports the ARM CortexTM-M3 microprocessor. Also, Express Logic and Interpeak announced that the companies have integrated Express Logic’s ThreadX RTOS and Interpeak’s TCP/IP stacks.

QNX Software Systems announced a new operating system extension that allows developers to build hardened, secure compartments around their software applications while providing the flexibility to maximize CPU resources.

QNX Wins Award at Embedded World

QNX Software Systems today announced it was named a winner of the prestigious Embedded Award 2006 at the Embedded World conference. A panel of judges selected the QNX® Neutrino® Multi-Core Technology Development Kit (TDK) as the best product in the software category for its outstanding technical innovation in embedded technology. This is the second time QNX Software Systems has won the Embedded Award. In 2004, the company was recognized for the groundbreaking architecture of its power management framework.

Monday, February 13, 2006

Oracle to buy Sleepycat?

In this weekend's Wall Street Journal there are rumors of Oracle buying a number of companies including JBoss, Zend and Sleepycat. Sleepycat is the commercial supplier of BerkeleyDB - an open source embedded database.

Friday, February 10, 2006

Esmertec Moves Beyond the Client

Esmertec (SWX: ESMN) has acquired a company that will help it address the entire mobile phone value chain with enhanced capabilities targeting carriers. The acquisition of Cellicium will provide the basis for the company's Mobile Operator Division.

We just got off the phone with a major equity analyst who wanted to talk about the Linux and Java businesses. Then we saw this release. From our perspective, the mobile Java business comes down to just a couple of companies with Esmertec being one of them. But client side Java can be tough business, companies in this market need to add value around the JVM either on the client or up and down the carrier value chain. It is not enough to just deliver a JVM. With this move Esmertec is working on the later.

Highlights from the release:

Cellicium, founded in February 2001, operates in Bagneux outside of Paris and is a premier provider of mobile browsing solutions, applications and related services to mobile operators. In the new division, Cellicium will continue delivering these carrier-grade solutions and services to GSM operators.

Jean-Claude Martinez, President and COO of Esmertec, has been appointed to take on the additional responsibility as President of this division, effective immediately.

Esmertec has taken a 100% equity stake in Cellicium. The initial purchase price is approximately EUR12.5 Million in cash, with an additional estimated EUR9.5 Million conditional payout in 2006 and 2007. The payout is based on earn-outs, of which 70% will be in cash and 30% in Esmertec shares. Cellicium is a profitable and cash flow positive company.

Thursday, February 09, 2006

Microsoft Ups Its Indemnification Package

The full release is here.

Highlights:

The strengthened IP protection will be available worldwide to Microsoft’s mobile and embedded partners and will include the following:

•The defense of OEMs and distributors against IP claims in every country in which Microsoft distributes or markets its Windows Mobile and Windows Embedded products

•Protection of patent, copyright, trademark and trade secret claims based on Windows Mobile and Windows Embedded software

•Removal of the monetary cap related to defense costs

VDC's View:

IP protection is certainly an issue assessed by OEMs employing embedded Linux. Over 60% of the OEMs using embedded Linux surveyed by VDC perform an IP risk evaluation. However, any concerns about IP risk do not appear to be substantially slowing embedded Linux adoption. Whether it is the existing IP indemnification programs offered by Linux vendors and others or a general lack of concern over the risks, OEM adoption is so widespread that Linux consistently ranks as the leading embedded OS in VDC surveys.

This announcement signals an extension of Microsoft’s indemnification program and further mitigates the risk to OEMs of Microsoft introducing patented technology into its Windows Embedded Platforms. The lawsuit filled by Visto in December 2005 against Microsoft shows that disputes over patented technology can come from a number of directions in the mobile and embedded software market. Although Visto is not currently going after Microsoft OEM licensees, the fear is that at some point it might - much like what SCO is threatening for users of Linux.

The real danger here, in my opinion, is an injunction or other ruling preventing an OEM from deploying that software on its devices or creating uncertainty about future availability. NPT’s lawsuit against RIM has resulted in a number of industry watchers counseling about the risks of deploying RIM devices. Microsoft has addressed the injunction issue in its indemnification package, however its remedies will take time to engineer or negotiate. Of course, with shrinking product cycles being the norm in the embedded systems industry, time is the real enemy.

This announcement seeks to shift the balance in software platform selection in Microsoft’s favor by planting small seeds of doubt in the minds of developers and risk evaluators at OEMs. It is just one more way in which Microsoft has differentiated itself vs. open source/Linux. Is this a huge announcement? No. But it should be seen within the context of Microsoft’s other strategic efforts to set itself apart from the open source model.

Clearly Microsoft continues to see open source - and in particular Linux - as its most important embedded competitor. And it should.

Wednesday, February 08, 2006

VDC in BusinessWeek Article

FEBRUARY 6, 2006

Open Source's New Frontiers

By Sarah Lacy

MontaVista's Uncertain View

This startup, which embeds Linux in consumer electronics, is poised for big growth and maybe an IPO -- if Wind River doesn't spoil the party

Jim Ready, CEO of closely held software maker MontaVista Software, started off 2006 relaxed from a Hawaiian vacation and espousing an upbeat outlook. His company, which specializes in code that's "embedded" in consumer electronics and other gear, was entering its seventh year. And Ready was confident that in 2006 MontaVista would turn profitable and possibly move closer to an oft-rumored IPO. "When we started this company, we knew this would change the embedded computing world, and that has happened at a pretty good clip," Ready says.

Bold words for a man who's currently undergoing a search for his replacement, has recently accepted the resignation of his marketing chief, and is in the midst of a restructuring that calls for an undisclosed reduction in staff. None of that is uncommon in the rough-and-tumble world of emerging tech companies. But Sunnyvale, (Calif.)-based MontaVista has a reputation for results that don't quite live up to outsize goals. And as rival Wind River Systems (WIND ) begins treading on MontaVista's turf, pressure on Ready and his team to make good on promises has never been greater.

ANOTHER RED HAT? At stake: how big a slice of the $1.5 billion embedded-software market will end up with MontaVista, which has hitched its fortunes to Linux, the low-cost operating system that's updated by developers around the world via the Internet. Ready's model is Red Hat (RHAT ). Just as Red Hat sells and supports Linux for companies, MontaVista develops and supports a version of Linux that's sold to engineers working on a vast array of manufactured products, from phones and to telecom equipment to cars and other consumer devices.

It's not hard to see why MontaVista -- or any other budding open-source company -- would emulate Red Hat. Sales at Raleigh (N.C.)-based Red Hat jumped 44%, to $73.1 million, in its fiscal third quarter, which ended in December. Net income more than doubled, to $23.2 million, in the same period. But Red Hat is the exception -- not the rule -- among open-source players.

MontaVista wants to change that. The market for embedded software is poised to boom.

Currently, many would-be customers write their own code in-house. But that can be costly. And a growing number of manufacturers would rather rely on a standardized operating system, freeing engineers to focus on the concepts that can really distinguish a product, such as design and layout. MontaVista and Alameda (Calif.)-based Wind River both reckon the embedded market could become as big as $5 billion a year over time.

BIG OPPORTUNITY. And Linux has obvious benefits. For one, it's often cheaper than proprietary alternatives. Also, manufacturers don't want to be locked into an operating system over which they have little control. Nor do they want to be beholden to any one vendor, as many computers makers are with Microsoft (MSFT ) and its Windows operating system.

Little wonder that Linux is finding its way into more devices. Motorola (MOT ), Samsung, and Panasonic have all introduced Linux smart phones (see BW Online, 11/8/05, "Linux Answers Phone Makers' Call"). The Open Source Development Labs has embarked on several projects to standardize Linux for wireless handsets and telecom gear.

It has the makings of a big opportunity. When Ready was getting started in 1999, using Linux for devices was a radical idea. John Shoch of Alloy Ventures remembers getting the call in 1999 when Ready first proposed an embedded Linux company. It hadn't even occurred to Shoch, though he had made several investments in embedded software.

"I wish I'd thought of putting those two words together," Shoch says of "embedded" and "Linux." "On the spot we shook hands [on an investment deal]. We didn't know how to sell or execute or meet the needs but knew this was a whole new opportunity and we were going to figure it out."

"TRUE COMPETITOR." And figure it out they did. MontaVista, with soaring growth rates, outmaneuvered several small competitors in the early part of the decade. But that growth has tailed off in recent years, analysts say. The private company doesn't disclose revenue figures. But analysts say sales are in the range of about $30 million to $40 million a year. Ready says growth was about 20% last year.