FSMLabs continues to add customers and win business for its real-time Linux products. Samsung Heavy Industries is using RT Linux Pro in its shipbuilding robots. Move over Roomba and Scooba the previous most high profile Linux Robots.

Friday, March 10, 2006

Timesys signs up Linux developers

Timesys reports that it has signed up 2,000 developers for its LinuxLink service. LinuxLink is a repository of the latest packages, development tools and other types of community support for Embedded Linux.

Could this signal an upsurge in the use of non-commercial distributions? Perhaps. But it maybe it just signals a change in how those existing developers acquire patches and tools.

Thursday, March 09, 2006

WIND Q4 - VDC's View

Despite the hit that Wind River has taken in the market (down 20% at 2pm), its Q4 and FY06 earnings have many positive components including:

- 1st Quarter over $70 million in 15 quarters going back to Q4 2002.

- Overall Growth of 13% and deferred revenue growth of 27%.

- $50 million in cash flow.

- Many big design wins, especially in military/aerospace.

So what did Wall Street investors not like about the numbers:

- The company missed the low end of its guidance of $72-74 million by turning in a $70.2 million Q4.

- Lower than expected Q1 guidance of $65-70 million or $0.34 to $0.39 per share less than analysts' $0.47.

Other factors to consider in evaluating the numbers:

The transition from paid up front product licensing to a subscription business model will not be always be smooth. In fact, there will be some jumps and some lags in it. This quarter was a jump. More of WIND’s business came in under the subscription model than was expected. Some OEMs in markets that typically prefer PUF, including military/aerospace and industrial automation opted for subscription. Has the inflection point been passed? Not by any stretch but OEMs appear to be considering alternatives to PUF growing numbers.

It appears that some bookings that were expected to be recognized because they would be under the paid up front licensing model were actually puchased under subscription models. Although this hurts WIND in terms of quarterly performance, this is better for the company in the long term. Subscription deals tend to:

1. Be larger deals

2. Lock in customers for the long term

3. Be renewed at higher rates than PUF

4. Include more products and services

5. Be standardization deals

Also mentioned were a number of deals that have yet to hit balance sheet that VDC believes to be quite large.

Bottom Line:

Certainly WIND missed its expected revenue number for the quarter, however there appears to be a number of mitigating factors including growth, cash flow, a movement to customers into subscription licensing which is better for WIND, and a number of deals that have yet to appear in the financial statements. WIND’s results are not simple to understand. They are neither all positive, nor all negative. There are no straight lines here, instead you need to look at all of the information. For VDC, the preponderance of that information is positive.

Wednesday, March 08, 2006

Wind River Post Healthy Gains But Misses High End of Guidance

Analysts had expected the company to earn $0.12 per share on revenues of $74.20 million for the quarter.

Full-Year Highlights:

Reported revenue increased 13% year-over-year to $266.3 million

Deferred revenue increased 27% year-over-year to end at $98.3 million

Non-GAAP earnings per share of $0.29 and GAAP earnings per share of $0.26

Non-GAAP cash flow from operations of approximately $51 million, excluding restructuring related payments of $1.8 million; GAAP cash flow from operations of approximately $49 million

Fourth Quarter Financial Highlights:

Reported revenue increased 11% year-over-year to $70.2 million

Deferred revenue increased 12% sequentially vs. Q3 FY06

Non-GAAP net income of $10.3 million and GAAP net income of $10.3 million

Non-GAAP earnings per share of $0.11 and GAAP earnings per share of $0.11

Non-GAAP cash flow from operations of approximately $16 million, excluding restructuring related payments of $579,000; GAAP cash flow from operations of approximately $15.5 million

(Full VDC Coverage Tomorrow)

WIND Earnings today at 5pm

WIND's share price has been trending in February. Is this a sign of things to come? Not so fast. If you have the time, check in with the price at about 2pm or so (maybe 3pm). There is usually some movement around then...and that movement usually tells us the way things are going.

Tuesday, March 07, 2006

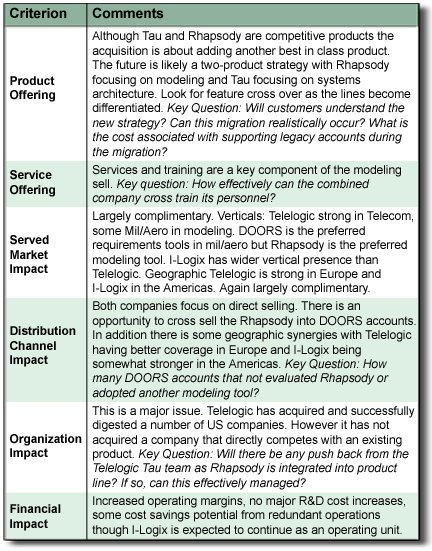

VDC's View Telelogic - I-Logix

The acquisition of I-Logix represents a continuation of Telelogic’s strategy to acquire leading companies in their respective corners of the application lifecycle management business. These acquisitions include:

Popkin (2005) - leader in enterprise architecture modeling (cost: $45 million)

QSS (2000) leader in requirements management tools (cost: $115 million)

Continuus (2000) leader in change and configuration management tools (cost: $42 million)

Other acquisitions include Verilog (SDL), COOL:Jex from Sterling Software (UML), Focal Point (decision management tool), Devisor (consulting) and Certeam (consulting)

Key observations:

I-Logix Rhapsody is likely the best-in-class software modeling tool. The acquisition brings another best-in-class tool into the Telelogic line continuing its successful acquisition strategy.

Telelogic’s transition from SDL to UML modeling has not been an easy one. While Telelogic has enjoyed great success in telecom, its move into other vertical markets has not been as successful. The acquisition brings instant credibility to Telelogic in the automotive, military and aerospace, medical and consumer electronics verticals.

The acquisition establishes the best-positioned modeling company in the embedded business from safety-critical, real-time applications to large systems architecture. The combination of Telelogic, I-Logix and Popkin is the “perfect storm” of software and systems modeling.

The acquisition brings together Telelogic’s strength in building product portfolios with I-Logix’s award winning product strategy. The key component that has been missing for Telelogic in its modeling products for some time.

This acquisition does not sacrifice the innovative relationship that I-Logix has established with Green Hills, which features a tightly integrated IDE/modeling environment.

I-Logix is also working on a partnership with Esterel Technologies to integrate Esterel SCADE certified code generator into Rhapsody. The result for military and aerospace customers could be a near-seamless experience from DOORS to Rhapsody to SCADE Qualified Code Generator (KCG) to Green Hills MULTI (certified by Esterel’s compiler certification tool), all running atop Green Hills’ INTEGRITY OS. Additional support comes from Enterprise Architect and SynergyCM. In addition to the end-to-end nature of the tool chain and the efficiencies of modeling, the benefits of this approach include compiler optimizations for faster, smaller code that is in essence certified by virtue of being generated by the certified code generator. VDC expects that other vertical markets will find this configuration appealing as well.

Bottom line: This is an important acquisition that benefits customers in a meaningful way while at the same time changing the competitive landscape of the industry. This is now clearly a 2-company market and Telelogic has the momentum.

Monday, March 06, 2006

Telelogic acquires I-Logix

What Happened:

Telelogic acquired I-Logix for $80 million in cash. The I-Logix team will form the basis of a new Systems and Software Modeling Division at the company. The new division will manage the Rhapsody, Statemate, Tau and Tau G2 products. I-Logix had sales of $26.8 million in 2005 and pre tax profit of $2.9million.

Embedded World Numbers are in

The participant numbers for Embedded World are in:

Exhibitors: 492

Attendees: 12, 234 (up 22%)

Speakers/Participants: 913 (up 22%)

Awards:

Software: QNX for QNX Multicore

Tools: pls Programmierbare Logik&Systeme for Universal Debug Engine

Hardware: NEC

VDC View: Embedded World continues to grow and maintain its place as the largest embedded trade show, but ESC West remains the most important. Could this change? Sure. But moving to San Jose is likely to boost ESC and help it maintain its importance.

Catch Us at ESC West

Chris and Matt will be at the show. If you would like to schedule time please drop us a line at the office. Email is best. Believe it or not, slots have already started to fill.

The Blog is Back!

On Target: Embedded Systems went to Maui for a couple of weeks and efforts to post from the island or from VDC Global HQ in Natick, MA were lacking. But we are back now. Tanned, Rested, Ready.

Subscribe to:

Posts (Atom)